Welcome to this edition of The Digital Enterprise, where we explore how technology leaders can turn digital ambition into measurable outcomes.

In this edition, I’m sharing insights from TDEOS Industry Research on Mid-Size Financial Services companies. We uncover the hidden crisis facing regional institutions as they rapidly lose market share to digital disruptors and outline a roadmap for how they can win it back.

A Silent Crisis in Regional Finance

Mid-size banks, credit unions, and regional insurers are under siege. While headlines focus on megabank mergers and crypto crashes, fintech startups are quietly draining away their most valuable customers. These digital-native competitors are faster, cheaper, and smarter, and they’re winning.

Despite investing heavily in technology, nearly half of mid-size financial institutions are still digitally underprepared. Our latest benchmark research reveals the true scale of the threat and the hidden opportunity to reverse the trend.

Who Are These Mid-Size Financial Institutions?

Mid-size financial services businesses represent the economic engine of regional America. These organizations include:

- Regional banks serving local and regional markets with $500M to $5B in assets

- Credit unions focused on member communities and small business lending

- Insurance companies providing specialized coverage for regional markets

- Investment and wealth management firms serving high-net-worth individuals and businesses

- Specialty lenders focusing on niche markets like equipment financing or real estate

Many started as community-focused institutions but have grown into national players while maintaining their relationship-driven approach. They pride themselves on understanding their customers’ unique needs and providing personalized service that large institutions can’t match.

These institutions have thrived over the past decade alongside the growing U.S. economy. Their regional focus and emphasis on small and medium businesses has positioned them well in markets where personal relationships still matter. However, this very strength their deep customer relationships built on trust and personal service is now under assault from digitally sophisticated competitors.

The Hidden Crisis

The threat isn’t coming from traditional competitors. Instead of losing customers to large national banks, regional institutions are hemorrhaging market share to fintech startups that have identified and exploited critical gaps in digital capability with surgical precision.

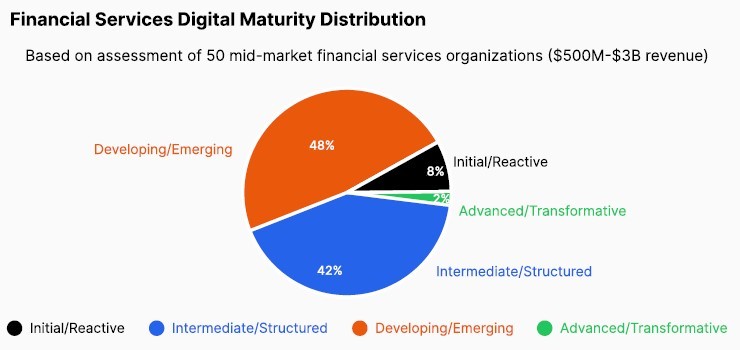

The numbers tell a stark story. Despite significant investments in technology infrastructure, only 2% of mid-size financial institutions have achieved advanced digital maturity, while 48% remain stuck in the developing stage, according to research from TDEOS.

This “Digital Value Gap” isn’t just about lagging technology, it’s about the fundamental ability to survive and thrive in an increasingly digital economy.

The Fintech Threat in Action

Mid-size financial institutions are caught in a perfect storm of digital disruption that threatens their very survival. Traditionally built on personal relationships and regional expertise, mid-sized financial institutions now face competitors who can approve business loans in minutes, issue insurance policies in seconds, and provide 24/7 digital services that their century-old systems struggle to match.

Consider the following examples of fintech disruptors:

Relay Financial exemplifies this disruption. Without being a bank itself, Relay has built a comprehensive banking platform specifically for small businesses, offering unlimited fee-free transactions, integrated expense management, and instant account setup. They’ve attracted thousands of small business customers who were previously loyal to their regional banks, simply by providing a superior digital experience that traditional institutions struggle to match.

Next Insurance demonstrates the devastating power of AI-driven customer acquisition. By using artificial intelligence to process small business insurance applications in under 10 minutes and offering 24/7 digital access to policies and claims, they’ve captured significant market share from traditional regional insurers. Even more concerning, companies like Intuit now use Next Insurance’s white-label platform to offer insurance directly to their customers, creating new competitive dynamics that completely bypass traditional distribution channels.

These fintech disruptors share characteristics that make them particularly dangerous to traditional institutions:

- Digital-first customer experience that meets modern expectations instantly

- AI and automation that eliminates traditional processing delays

- 24/7 availability through sophisticated, always-on digital platforms

- Simplified processes that remove friction points customers didn’t even know they hated

- Data-driven insights that enable rapid product innovation and personalization

Benchmark Findings: The Digital Maturity Gap

New benchmark research from TDEOS, analyzing 50 mid-market financial services organizations, reveals the true scope of the digital maturity crisis facing regional institutions. The findings should serve as a wake-up call for every executive in the industry.

The Devastating Distribution:

- Only 2% have achieved “Advanced/Transformative” digital maturity – these are the institutions positioned to compete effectively against fintech disruptors

- 42% remain at the “Intermediate/Structured” stage – functional but increasingly vulnerable to digital-native competitors

- 48% are stuck at the “Developing/Emerging” stage – significantly behind market expectations and customer demands

- 8% remain at the “Initial/Reactive” stage – facing existential competitive threats with outdated capabilities

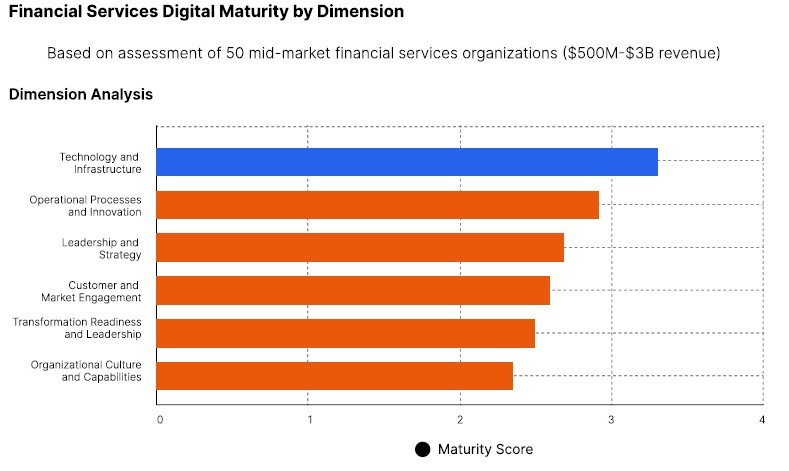

The Technology Paradox: Perhaps most alarming is what the research reveals about technology investment effectiveness. Mid-size financial institutions score highest in Technology Infrastructure (3.25/4.0), indicating substantial investment in systems and platforms. However, they score lowest in Organizational Culture & Capabilities (2.38/4.0), creating a dangerous paradox: institutions are spending heavily on technology but failing to realize its full potential due to organizational limitations.

This creates what TDEOS researchers call the “Digital Value Gap” – the disconnect between technology implementation and actual business outcomes that affects the vast majority of regional financial institutions.

Critical Capability Failures: The research exposes specific areas where traditional institutions are most vulnerable:

- Transformation Readiness (2.54/4.0) – Limited ability to translate digital investments into measurable business outcomes, leaving institutions vulnerable despite significant technology spending

- Customer Engagement (2.69/4.0) – While institutions have basic digital channels, they lack the integrated, personalized experiences that customers now expect

- Innovation Management – The research shows systematic weaknesses in how institutions identify, develop, and implement new digital capabilities

The $76M-$125M Value Opportunity Hidden in Plain Sight

For a typical mid-size financial institution with $1-5B in revenue, the TDEOS analysis identifies massive unrealized annual value trapped by the Digital Value Gap:

- Revenue Growth Potential: 15-20% increase through improved digital customer acquisition and retention

- Cost Optimization: 25-30% reduction opportunity through intelligent process automation and efficiency gains

- Customer Experience Enhancement: 35-45% improvement potential leading to dramatically higher satisfaction and loyalty

- Operational Efficiency: 30-40% enhancement through AI-powered digital process optimization

The stark contrast with high-performing organizations demonstrates what’s possible. The 2% of institutions achieving advanced digital maturity show:

- 22% higher revenue growth than their less mature peers

- 31% better customer satisfaction scores

- 28% lower operating costs

- 45% faster time-to-market for new offerings

The Path to Survival and Growth

Mid-size financial institutions face a stark choice: systematically close their Digital Value Gap or risk continued market share erosion to fintech competitors. Success requires addressing technology, culture, and operational capabilities simultaneously through a structured transformation approach.

Immediate Survival Actions:

- Conduct comprehensive digital maturity assessment to understand current position relative to industry benchmarks

- Implement Digital and AI-powered quick wins to demonstrate transformation capability and build momentum

- Accelerate cultural transformation to support digital adoption and innovation

- Establish value measurement systems to ensure digital investments deliver measurable business outcomes

- Create rapid innovation processes to match the agility of fintech competitors

Long-term Strategic Positioning: The most successful regional institutions will combine their traditional advantages of deep customer relationships, market knowledge, regulatory expertise, and comprehensive service offerings with digital capabilities that match or exceed fintech competitors. This hybrid approach leverages relationship strengths while eliminating digital disadvantages.

The Closing Window of Opportunity

The fintech disruption of regional financial services isn’t a future threat, rather it’s accelerating rapidly. However, traditional institutions still possess significant advantages they can leverage established customer trust, regulatory expertise, comprehensive service portfolios, and deep local market knowledge.

The critical factor is developing the digital maturity needed to deliver these advantages through modern, AI-enhanced experiences that compete effectively against digital-native competitors. Organizations that act decisively to close their Digital Value Gap will not only survive the ongoing disruption but position themselves to capture market share from less prepared competitors.

Those that delay risk becoming cautionary tales in the story of financial services transformation.

Take Action: Assess Your Digital Competitive Position

Get the Complete Financial Services Digital Maturity Benchmark Report Access the full research findings, including detailed industry analysis, maturity frameworks, and transformation roadmaps specifically for mid-size financial institutions.

👉 Download the Complete Report

Discover Your Organization’s Digital Maturity Score Take the comprehensive Digital Enterprise Maturity Assessment to understand exactly where your organization stands compared to industry benchmarks and receive a personalized roadmap for closing your Digital Value Gap.

👉 Take the Free Assessment – Know Your Digital Readiness

Includes:

- Detailed comparison against industry benchmarks

- Identification of high-impact improvement opportunities

- Customized transformation roadmap

- Complimentary consultation with TDEOS experts

This analysis is based on proprietary TDEOS research into financial services digital maturity. The complete benchmark study analyzed 50 mid-market financial services organizations across six dimensions of digital capability.

About TDEOS: The Digital Enterprise Operating System (TDEOS) is a comprehensive framework for accelerating digital transformation and closing the Digital Value Gap. Our battle-tested approach combines strategic assessment, organizational development, and implementation support to help enterprises navigate complex digital challenges and capture transformation opportunities. Founded by an industry veteran with 22+ years of Fortune 500 transformation experience, TDEOS has helped organizations achieve 2-3x higher returns on digital investments while accelerating time-to-value by up to 60%.